Saturday, July 27th, 2024

David Drennan

My experience of job descriptions is that they are brought out to explain the job to some new employee, or dragged out for a job evaluation exercise, but otherwise they sit neglected and forgotten in a drawer somewhere. That's because they are inert, passive documents, often used once and then discarded. They may show who the job-holder's boss is, what department they are in, who their contacts are, describe their activities, but they do nothing to energise the business.

The trouble with job descriptions is that they only describe activities. Most are full of “-ings” : plann-ing, organiz-ing, communicat-ing, decid-ing, motivat-ing, etc. etc. What we need to describe are the outputs required of the job-holders, so that they know what to focus on, what to spend their time on, how to get the right things done. A powerful new trend today is to describe jobs not as a series of activities, but in terms of the Personal Contributions (PCs) each job-holder can make to the performance of their company.

The first rule when defining the PCs of any job is:

- They should represent the outputs of the job, the results to be achieved rather than the activities used to achieve them

Take a sales representative job as an example. In describing their job, a salesperson might say : “I research my territory; I make phone calls to make appointments; I travel to meet potential clients; I make presentations”, etc. But these are all activities, they only add cost. The only thing that adds value to the business is ‘actual sales’, and that should be the first output of virtually every salesperson job. One of the key tasks then is actually to minimise the number of activities it takes to achieve real sales, the key reason the individual is employed. That is what makes the salesperson truly productive.

Take another example : a maintenance engineer. Asked to describe his job, he might say : “I work with tools; I attend to breakdowns; I keep spare parts; I carry out regular oiling and greasing services”, etc. And while all these may be needed, again they are all activities, they only add cost. The true output we are looking for, and what the engineer should focus on is : ‘Fully Operational Equipment’. We should then help the engineer minimise the effort and cost involved in delivering that result.

When maintenance engineers have their jobs defined as a series of outputs rather than a list of activities, they not only begin to see their job differently, they start doing it differently. Often they stop calling their job ‘Breakdown Maintenance’ (we only work when machines break down) and rename it ‘Running Maintenance’ (our job is to avoid breakdowns and keep things running). They soon realize that showing machine operators how to avoid the most common breakdowns makes the job easier for both parties. That stimulates co-operation between engineering and production rather than conflict (never an easy thing to do!).

And that is one of the great benefits of describing jobs in terms of Personal Contributions. People begin to understand that they are not only doing a job, but that that job needs to be making a positive contribution to the profitability and effectiveness of the organisation as a whole. PCs, by focusing on the outputs of the job, also make it clear just ‘who does what’, so that (like the engineers and production operators above) staff in different departments can integrate their activities and work like a team to get a better job done.

The second rule about Personal Contributions is :

- They should be unique to the job-holder

Fuzzy responsibilities can cause wasteful overlap and duplication in many companies. That adds cost but no extra value. PCs start from the premise that where two people are responsible for the same thing, one is not required. Indeed, where three people are responsible for the same thing (and it often happens), two are not required. PCs make clear what each individual is uniquely responsible for, and how their work interlocks with those of their colleagues. Similarly, jobs at every level have to add some new value, not simply supervise the jobs of others.

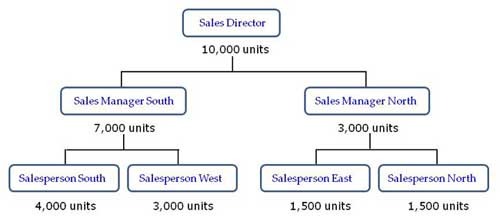

Let's take an example. It is not uncommon for sales organisations to decide on overall company sales targets, and to allocate subdivisions of this to the various regions or departments involved, who in turn allocate targets to the front-line salesforce. In simplistic terms, this might lead to an organisation chart like the one below :

PCs say there is only one group of persons responsible for making sales, namely the salespersons who come face-to-face with the customer. That is their unique responsibility. It is not enough then for managers to claim their job is simply to encourage, push, pressurize and otherwise ‘motivate’ their salesforce to meet their targets. If the salesforce are already meeting their targets, then we don’t actually need any of the managers above . . . unless they add new value. So what is that new value?

Let's rewrite the jobs in terms of their Personal Contributions. For salespeople, we might decide on Sales Levels (actual versus target), Order Size (to prevent too many overly small orders), and New Accounts (to broaden the customer base) as three of their key PCs.

What contribution could Sales Managers then uniquely add? Here we could nominate Sales Tactics (developing strategies for maximising sales), Sales Training (organising for salespeople to get the training they need), and Sales Administration (minimising the amount of admin. salespeople have to use to get the job done). In other words, Sales Managers become the ‘servants of their people’ rather than their supervisors. Supervising the work of a subordinate is an activity, not an output.

At Director level, we would attribute PCs where they have unique authority to act. For example, Company Sales Strategy (deciding for example which sections of industry the company should focus on), Sales Prices (decisions which help the company maintain margins yet stay competitive), Market Research (such as working on ideas for new products, etc.).

The organisation chart might then look more like this :

The list at each level is likely to be longer in a real situation, of course, but the layout illustrates the key points. Every PC is unique to the person at that level, there is no repetition or duplication. But the PCs are specifically designed to work together to form a coherent whole, where everyone knows clearly what the others role is, and each can support the other in maximising the performance of the organization as a whole.

Fuzzy or overlapping responsibilities can often be annoying and confusing, but in some cases they can be downright dangerous. This came home sadly to one company when a contractor was electrocuted on the job, and managers started blaming each other for the failure. The Maintenance supervisor had not controlled the job, some said; the Maintenance supervisor said the blame lay with the electrician who last worked on the equipment; surely the Production Director must be accountable for everything that happens in his area, said others; the Safety Officer did not ensure the situation was safe, said the Production Director. When tempers had cooled, it became obvious the responsibilities on safety had to be made much clearer for the future.

Managers in every area had to take on personal responsibility for providing equipment which was safe for staff to operate, they concluded, but equally staff members had to adopt safe working habits to make the system work effectively. The Production Director had both the responsibility and the right level of budget authority to provide a safe working environment. Equally, he had to ensure the work arrangements met laid-down legal requirements, even though he would take advice on that subject from the Safety Officer, whose personal responsibility it was to keep fully up-to-date with current legislation.

The interlocking responsibilities then began to look like this :